While management teams are often not correct on their views expressed during conference calls, important market intelligence through common themes can be gathered by listening carefully. A summary of ten topics (only nine are important) on the global deepwater oil and gas market are discussed this week:

(1) Will drillers update guidance for project commencements in 2H2025-2026 noted in prior quarters? Idle time is a reality for some rigs in 2025 but do they see additional slippage on projects? I believe there’s risk of additional delays although should be modest. Why? Eni announced this week it is delaying its decision on Baleine Phase 3 in Cote d’Ivoire from early 2025 to mid 2025, although Baleine has been very successful thus far so its a question of when not if.

FPSO supply chain and equipment delays have contributed to idle time risk on rigs. Global supply chain was gutted in the downturn (2015-2022) and ramping up having some challenges. There are only a few subsea equipment providers today (TechnipFMC) — will we see more competition in future years?

Christmas trees are an example of subsea equipment delays. A Christmas tree in subsea oil and gas is an assembly of valves, spools, and fittings installed on a wellhead to control the flow of hydrocarbons. It regulates production, injection, and pressure while enabling safe well intervention

(2) The big picture question on the drillship market, particularly in relation to multi-year development drilling projects, is whether we will see:

(i) a continuous delay in project commencements, with timelines consistently pushed further out, or

(ii) a call on rig demand concentrated within the 2027–2030 period.

On Friday, Chevron spoke positively about its deepwater E&P portfolio, which I believe underscores the importance of exploration. These projects provide IOC’s long-term optionality, allowing them to select the best projects across jurisdictions. However, capex investment competes with shareholder returns, limiting demand growth to varying degrees by IOC. If multiple IOCs require additional drillships in the late 2020s, dayrates could surpass $600K, with timing playing a critical role.

I believe we see strong demand into the 2027-2030 period although global oil and gas prices will play a role in how this market plays out.

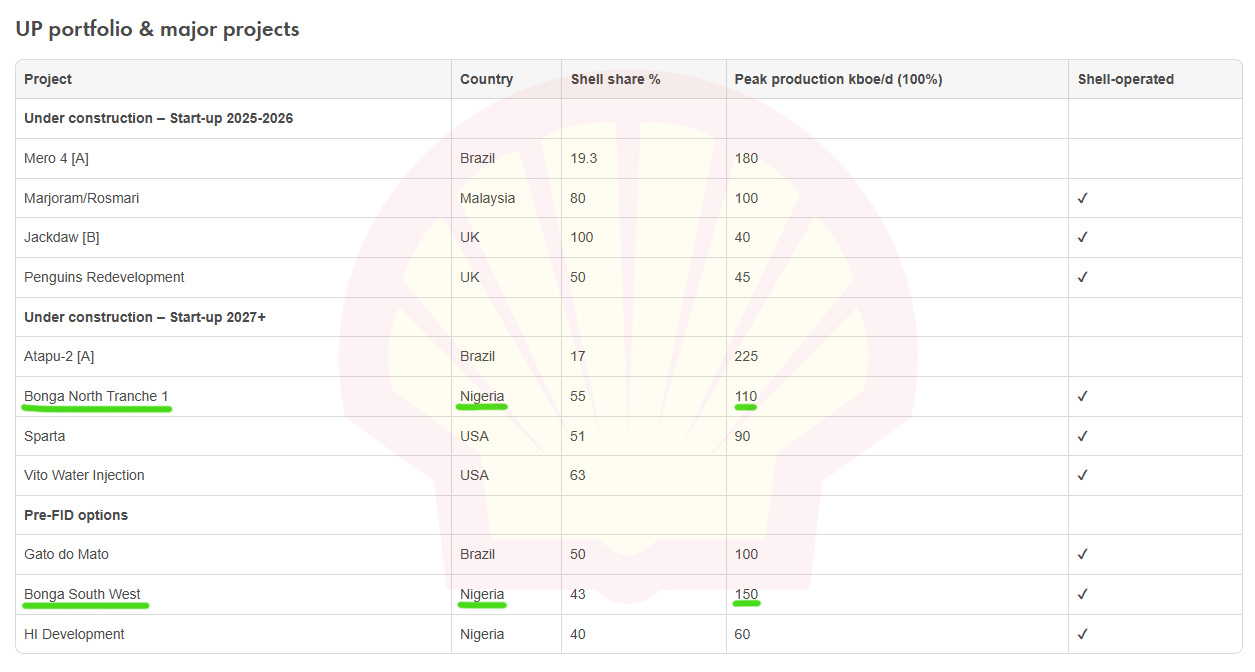

(3) Shell’s Namibia Write-Down Impact on Rigs: I follow Namibia exploration closely due to its potential impact on the rig market toward the end of the decade. Shell recently announced its discoveries in Namibia were not economic for them to develop. I believe the discoveries made by TotalEnergies and Galp Energia are higher probability project sanctions, along with potential for Rhino/Azule in PEL 85.

Shell reached final investment decision on Bonga North in Nigeria, although wrote down its Namibia discoveries. It would be great to see demand for both Nigeria and Namibia, but drillship demand for Bonga North is closer. The market values more near term demand, and while Shell hasn’t been firm on dates with Bonga the wait won’t be as long as with how their Namibia discoveries were projecting.

(4) Nigeria’s Importance to Drillship Market: Delays in Nigerian project commencements have contributed to the current softness in the drillship market. Initially discussed in 2H 2023, these projects do not yet have firm timelines. Shell’s Bonga FID is a positive development, while key projects from ExxonMobil, Chevron, and TotalEnergies are expected to proceed in time. Concurrent drillship demand (4 to 5) from these projects would be beneficial to the drillship market, but timing remains uncertain, with some final investment decisions still pending. Nigeria is an important market to follow in 2025-2026.

(5) The semisub market in Norway remains healthy with Equinor exercising an option last week on Odfjell’s Deepsea Atlantic at a ~$500k dayrate. I expect this market to remain healthy in coming years. We are likely to see some variance on dayrate announcements in 1H 2025, as stated in my Offshore Credit outlook a few weeks ago;

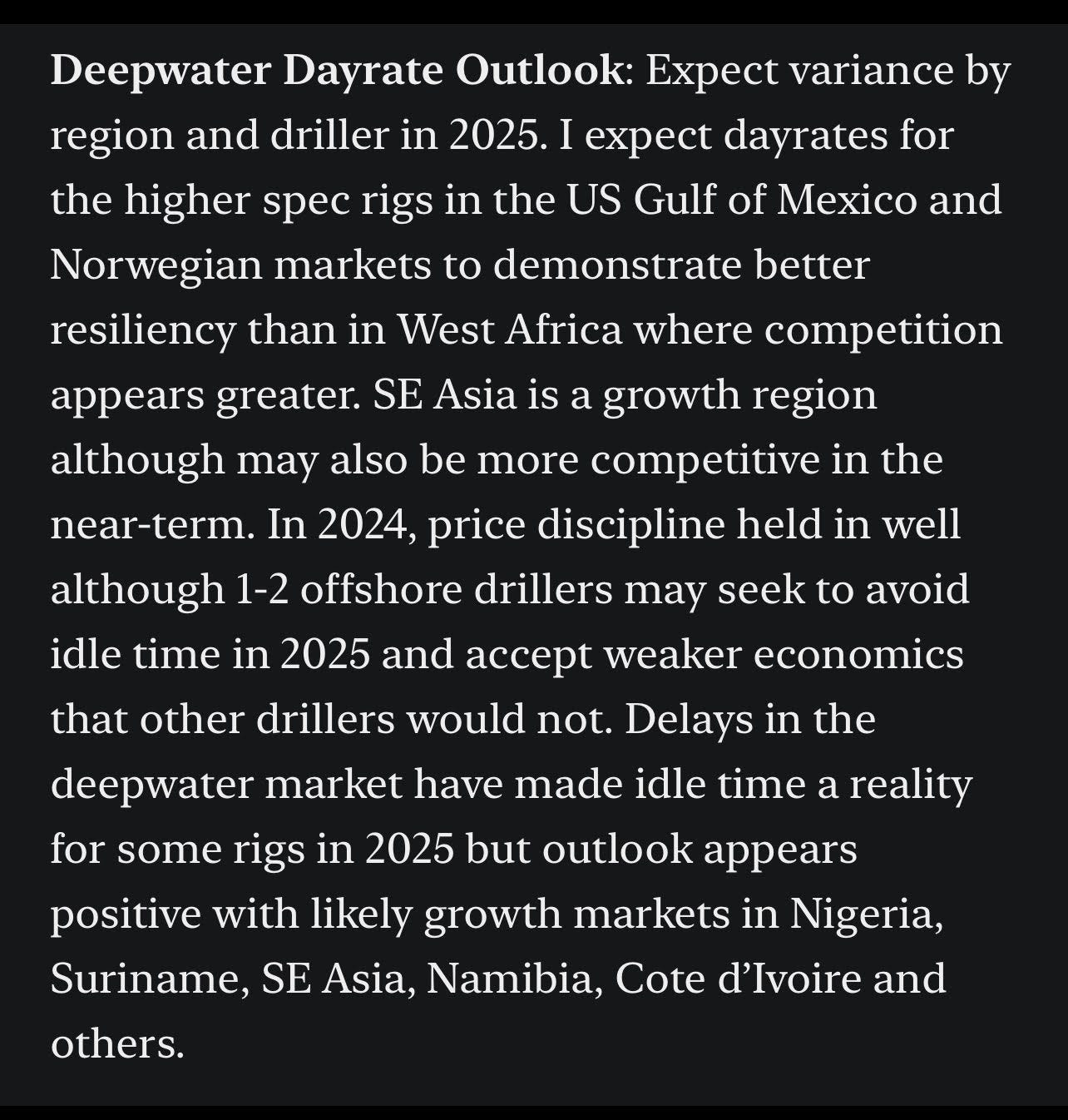

Drillship market may face some bids for utilization to avoid warm stacking costs in certain regions. While still to be seen, I expect more resiliency in the US GoM market on dayrates and potentially softer data points in West Africa and SE Asia for 2025

(6) Rosebank: This week the Court of Session in Scotland ruled the Rosebank deepwater project in approval was given unlawfully due to its lack of consideration for specific environmental impacts. Despite this ruling, the project appears to still be moving along while additional approvals are required. If there are delays tied to Rosebank, Equinor is likely to use Deepsea Atlantic in Norway which may crowd out a rig for an unknown period of time. I believe the Norway semisub market is healthy and impacts would be limited although it might crowd our SFL’s Hercules (currently idle) for a longer period of time, perhaps forcing it to another region long-term such as returning to Namibia.

Rosebank will have a very experienced North Sea E&P operator (Equinor/Government of Norway) with a recently upgraded Ultra-Deepwater Harsh Environment Semisub, Odfjell’s Deepsea Atlantic. As a 70% state-owned oil company, Equinor invests billions in uneconomic renewable energy projects with low-mid single digit IRR’s which receive funding support through economic returns from oil E&P. Equinor is arguably the most ESG-friendly large oil and gas company in the world and a good operator to have on this project.

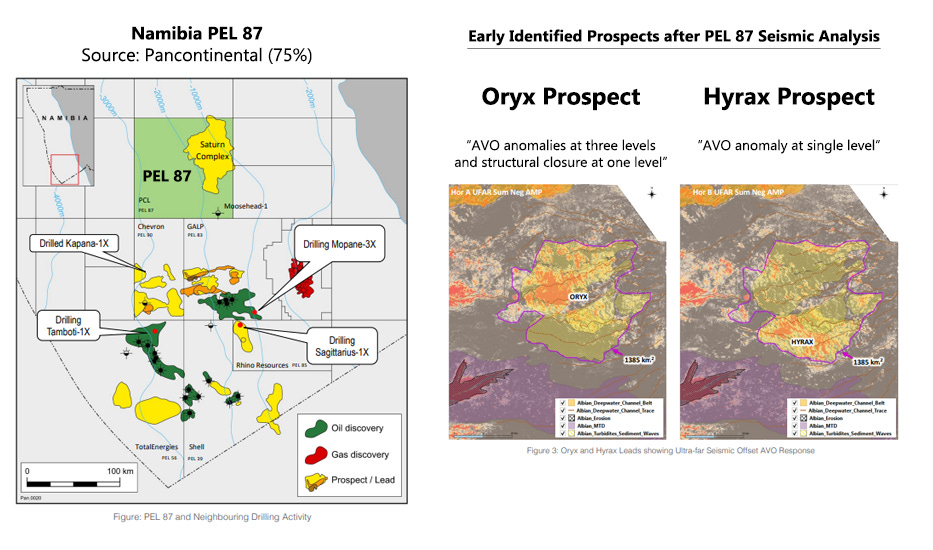

(7) Namibia Deepwater Exploration: TotalEnergies should provide an update on its Tamboti-1X well in Namibia. Given that TotalEnergies has not yet sanctioned a project in Namibia, I would expect a watered down update on Tamboti-1X. The enthusiastic quotes about the exploration well were surprise at the Strategy Day in October. TotalEnergies’ Venus discovery appears as a likely project sanction sometime in the next 12 months. TotalEnergies likes scale so having a brownfield expansion option for another FPSO at Mangetti and/or Tamboti would support FID on Venus. TotalEnergies also has additional Orange Basin prospects they’ve yet to drill in both Namibia and South Africa.

There’s no shortage of exploration prospects in Namibia. Pancontinental Energy provided interesting detail on two prospects (Oryx and Hyrax) in its quarterly update this past week:

Some current exploration wells are adjacent to other blocks. Rhino/Azule’s Sagittarius-1X is possibly drilling an extension of PEL 83’s Mopane discovery into PEL 85, so success there could have implications for Galp in PEL 83. Chevron’s Kapana-1X well was uncommercial but was further away from TotalEnergies’ Mangetti discovery than I thought their first well would be. Chevron’s comments on 4Q24 call indicated they may have an appetite for more exploration in PEL 90, so if TotalEnergies’ Tamboti-1X is successful it may provide valuable info for Chevron on nearby targets in PEL 90 considering the proximity of Tamboti to PEL 90.

(8) Jackup Credit Quality: Shallow water jackup rigs have seen weakness in high yield credit markets due to jackup rig suspensions, mainly tied to Saudi Aramco. Borr recently converted past due Pemex receivables to cash in a factoring transaction. While this was positive development for their liquidity, contracting progress for 2026 and beyond will be a key item to follow in coming quarters.

Borr’s secured notes have widely split credit ratings: S&P is B+/Stable and Moody’s is B3/Positive. Given the ~10% YTW on the secured 2028s, at or below par, these may be a good opportunity for a CLO manager to utilize its bond bucket if it has appetite for offshore rigs (most do not!), particularly if they have room on their Moody’s “Caa” bucket given Borr’s “B3” rating.

(9) 7G Upgrades? NOV’s 3Q24 call noted that a client booked two hookload upgrades to convert 6G drillships to 7G drillships. It’s not clear who this client would be, but Stena has two recently idle 6G drillships (Drillmax and Forth) so would be possible candidates for this work. This would be an expensive upgrade that I’m not sure would make sense for other drillers to do. Stena has a 6G heavy fleet so would be a logical candidate for this upgrade although is only speculation on my end.

(10) Gulf of America? Kind of a silly topic but Chevron referred to the “Gulf of America” on its conference call on Friday. Will be interesting to see if other American oil and gas companies do the same in coming weeks.

Thanks Tommy 👍