Summary: (1) How changing future oil production sources are likely to impact the structure of the global oil market, (2) A constructive deepwater rig orderbook picture and (3) an alternative income stock to high yield with a more balanced risk/reward profile.

Evolving Structure of the Global Oil Market

The Permian Basin has been a blessing to the US economy after adding >4.5 million bpd over the last decade. The Permian has two primary sub-basins: the Midland Basin (area around Midland, Texas) and the Delaware Basin further west which extends into SE New Mexico. The Permian’s growth was most pronounced in 2017-2019 due to growth in the more oil-weighted Midland Basin (Pioneer Resources’ backyard), whereas in years following has slowed as drilling and completion activity grew in the more gassy Delaware Basin.

Debate exists about Permian oil production and its future trajectory. It’s growth has slowed although has been more resilient than I expected 12 months ago. There’s a lot of smart people in Texas with good technology but Permian production is trending toward higher gas and NGL mixes per well along with increasing costs per barrel of oil produced. I expect modest resiliency from Permian production but it is a maturing basin.

In 2015-2017, US onshore oil production had a more advantageous set-up than global deepwater as E&P capex favored Permian production given its lower-cost (at the time), short-cycle nature for faster payback and more flexible spending. Back in 2015-2017 when WTI oil prices were range bound between $40-$60/bbl, if WTI hit $60/bbl, EOG, Pioneer, Continental and other Shale E&P’s could call Halliburton to complete “drilled but uncompleted” wells and be producing new barrels in months with good returns. That is “short-cycle” US Shale capex.

As the Permian’s Tier 1 oil well inventory shrinks and as service companies demand adequate returns, costs have increased. Shale capex seems to face restraint when WTI falls below $70/bbl today although depends on various other factors. In 2015-2019, IOC’s and E&P’s had a clear preference for flexible US shale capex as they repaired the balance sheets they leveraged when oil was ~$100/bbl during 2011-2014. IOC’s and E&P’s have better balance sheets today than a decade ago and are in better positions to invest in larger, less flexible, longer-term projects.

Future Incremental Barrels will be Less Flexible

As US Shale matures, it begins gradually handing the baton to Deepwater sources of energy to offset natural oilfield decline and (potentially) growing global demand. Deepwater E&P has a very different capital investment profile from US Shale. Deepwater E&P capex is larger financial commitments as recent project sanctions have ranged between 70k bpd (Kaminho in Angola) and 220k bpd capacity (GranMorgu in Suriname).

GranMorgu is a multi-year, $10.5B capex project with these barrels mostly hitting the market in 2029 whether Brent crude is $50/bbl or $100/bbl at the time. Deepwater E&P is “long cycle” whereas “short-cycle” US shale capex can flex up and down depending greater on oil prices at the time. US Shale can still flex up if WTI >$85/bbl if the market needs the barrels but I expect additions to the global oil market will likely become more lumpy and lagging oil prices at time of FID in the next 5-10 years via lower cost per barrel deepwater growth.

Argentina’s Vaca Muerta is also an important source of future oil production. I believe infrastructure constraints may limit its growth potential but along with deepwater E&P, Vaca Muerta is also a relevant economic source of future oil production.

The chart below represents only ~10% of global oil production, although I believe is emblematic of the challenges the deepwater services market experienced from 2015-2022. Permian production arguably played a role in crowding out deepwater E&P capex in West Africa (represented by Nigeria and Angola). Nigeria and Angola have lost approximately 1.2 million bpd of production over the past decade due to various reasons, notably including underinvestment in deepwater E&P. Nigeria and Angola stopped the bleeding in 2023 and have multiple projects with major IOC sponsors for growth through the end of the decade. Nigeria and Angola have their own unique circumstances although are important deepwater E&P markets, in addition to Brazil, Guyana, Namibia, Suriname, Cote d’Ivoire and various other countries.

Permian and West African oil production growth aren’t mutually exclusive, although slowing Permian production would be a factor in supporting global oil prices and a contributing factor in future deepwater project sanctions.

Deepwater Rig Orderbook is Much Improved

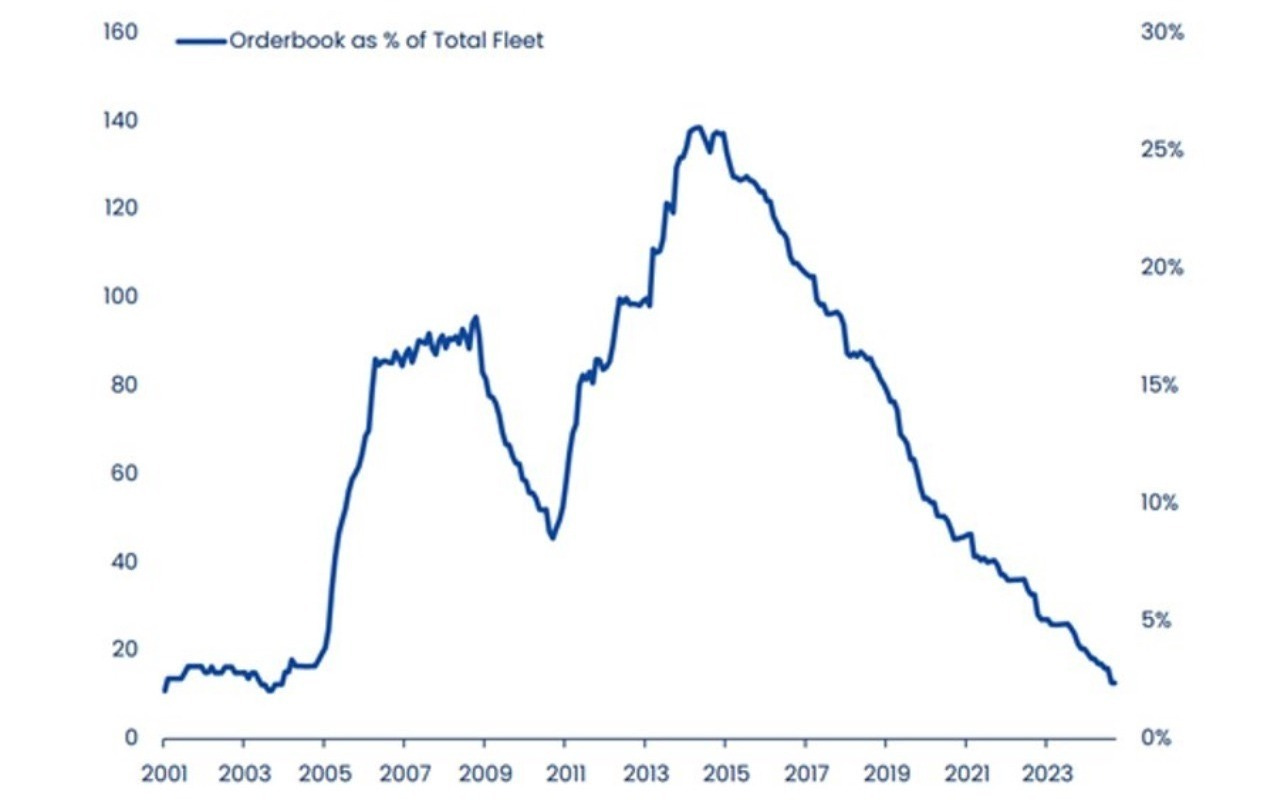

The deepwater downturn of 2015-2022 was not just due to Permian production growth, but heavily attributable to a very bearish deepwater floating rig orderbook from orders made in 2013-2014. Not only was offshore services demand poor due to Brent crude oil averaging ~$49/bbl from 2015-2016, but the market was staring at an unrelenting new supply of floating rigs for years to come. Since then, the market has rationalized a lot of the less efficient floater fleet and has absorbed much of the newbuild deliveries.

The chart above depicts the amount of deepwater rigs under construction in shipyards relative to the global fleet. The newbuild supply was a major problem from 2015 through 2022, although today is much healthier with no newbuild orders coming for many years to come. There’s no newbuild orders coming for the foreseeable future because they require dayrates meaningfully higher than $700k and multi-year term (5 years or greater). After nearly 10 painful years, deepwater floater supply has nearly worked its way through an overcapacity issue.

About 4-5 “stranded newbuild” 7G drillships still exist. While they may not find a home in West Africa if/when eventually contracted, demand picking up in countries such as Nigeria would play an indirect role in absorbing the last remaining stranded newbuilds. At the time of original orders, I recall optimism about pre-salt discoveries in Angola rivaling those in Brazil which was expected to support drillship demand (recall Cobalt International Energy). Those have mostly yet to materialize.

Noble Corp as a High Yield Alt

High yield ETF’s JNK and HYG have an average trailing yield of ~6.2% while the 5-year US Treasury bond yields ~4.4%. In high yield, you’re getting a tight credit spread carry and hoping no recession in 2025-2026. High yield is likely OK but there’s not much upside beyond the yield. New issue CLO “BB” notes have recently priced inside 500 bps (that ain’t cheap). Credit risk is expensive.

HY credit spreads are tighter today than they were in August 2021 when Carvana successfully issued $750mm of Senior Unsecured bonds at 4.875% with negative EBITDA and heavy working capital intensity. Those bonds were underwritten based on Carvana equity value, certainly not cash flows because they were quite negative at the time. To my surprise, Carvana’s equity value ended up being worth a lot but debt investors did not participate in that upside despite underwriting the risk. Debt investors received their credit spread compensation in Carvana unsecureds, however the downside was meaningful and upside was capped.

I don’t own Noble Corp shares (~6.1% div yield comparable to JNK and HYG) but its yield is comparable to high yield ETF’s and it has upside. Noble is arguably the most institutional investor friendly offshore contract driller. Why? It pays dividends, buys back shares, has adequate leverage and management has done a good job pricing its assets. Noble is an offshore contract driller with drillships, semisubs and jackup drilling rigs. They have a very good fleet of 7G drillships. I think their jackup rigs are good, semisubs are OK and they have recently acquired Diamond Offshore which should support $75mm-$100mm of annual synergies.

Consensus EBITDA estimates are ~$1.25B (2025) and ~$1.5B (2026). DYODD but annual capex ~$425mm, cash interest ~$160mm and minimal (if any) debt amortization leaves room to support ~$325mm of dividends, working capital fluctuations and utilizing their $400mm share repurchase program approved in October 2024. Noble also has meaningful net operating loss carryforwards with future tax shield benefits.

Noble’s shares faced pressure in 2H24 not only due to negative oil sentiment and its impact on service company valuations but concerns about rig idle time in 2025. In recent weeks, Noble has found work for Globetrotter I, Noble Developer and Noble Venturer at adequate dayrates averaging near $400k. Based on estimated values of their semisubs and jackup rigs, I believe the equity market is valuing their fleet of fourteen (14) warm 7G drillships below $300mm each. I’m comfortable conservatively valuing those 7G drillships at >$400mm each using various valuation methods. Newbuild costs are mostly irrelevant today but it’d cost >2x to build the same 7G drillship new, along with an unfavorable payment structure (large cash deposit).

Owning high yield is expressing a positive view on risk assets. If you’re looking at risk, you should have upside. Noble Corp is a volatile offshore drilling rig company with risk exposure but has a comparable yield to high yield ETF’s and you get upside potential you don’t find in fixed income if you’re willing to take oilfield services equity risk after poor performance in 2024. I wouldn’t be surprised if they coldstacked one of their lowest tier floating rigs but their overall fleet quality is good in my opinion.

Comparing Noble (NE) to high yield is great insight, with NE currently carrying a 6% dividend, along with a board approved stock buyback program. Thanks Tommy.

Any more M&A coming? Cheap assets all over the place and unlevered balance sheets ex-RIG?